- Scottish Based Firm

- 5 Local Offices

- Established over 25 Years

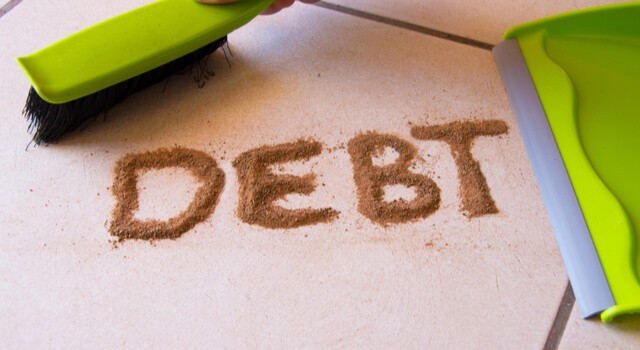

- Lower your Monthly Payments

- Write off a Proportion of your Debt

- Scottish Based Firm

- 5 Local Offices

- Established over 25 Years

- Lower your Monthly Payments

- Write off a Proportion of your Debt

- Scottish Based Firm

- 5 Local Offices

- Established over 25 Years

- Lower your Monthly Payments

- Write off a Proportion of your Debt

- Scottish Based Firm

- 5 Local Offices

- Established over 25 Years

- Lower your Monthly Payments

- Write off a Proportion of your Debt